With the payments industry increasingly going digital, fintechs and traditional financial institutions alike are exploring ways to harness technology to streamline many aspects of the payments industry. Underlying this digital transformation is open banking, the use of open APIs to build a range of products and services around financial institutions.

One area where open banking is driving innovation is payment hubs—integrated multiple payment systems that enable institutions to handle all aspects of the payment journey from a central point. Payment hubs leveraging open banking can make business easier, reduce friction, and drive more revenue.

To understand the open banking landscape, payment hubs, and what the future has in store, PaymentsJournal sat down with Lance Homer, Global Head of Digital Payments and Banking Ecosystem at Equinix, and Tim Sloane, VP of Payments Innovation at Mercator Advisory Group.

The Three Waves of Digital Transformation in Banking

The open banking revolution that the payments industry is in the midst of can be viewed as the third major digital transformation in banking, explained Homer. The first was during the 1990s, when the internet first penetrated consumers’ homes. This enabled banks to create websites where customers could check their balances and download transaction files, allowing them to utilize personal finance software such as Intuit.

Then in the 2000s, there was another breakthrough. As smartphones became ubiquitous, “banks began to develop their own banking apps or even wallets, and rather than having to visit a branch or ATM to deposit checks, consumers could take a picture of a check with their phone and use their phone to send and receive money through a banking app,” said Homer.

The 2010s marked a new transformation, albeit one that is still unfolding, as open banking began to take off. “We are very much still in the early days of this digital transformation,” said Homer. Unlike the previous transformations, which happened without prodding from the government, open banking has need a bit of a push from regulators, at least in Europe.

“Open banking in Europe is driven by PSD2,” explained Sloane, regulations which, in part, require banks to create access to consumer data via open APIs. But while the involvement of regulators makes this digital transformation different from previous ones, it’s not what makes open banking so transformational.

“What makes this wave so much more transformational is that consumers will be doing banking services beyond the typical bank-controlled channels, such as a branch, bank website or a bank app,” noted Homer. “It’s going to create competition in the market space for new innovation that in the end will give all the end users better experiences.”

The challenges of scaling open banking

Since open banking is still in its relative infancy, it is hard say with certainty what it will look like in a few years. However, there are some points worth considering. Homer explained that the current (and mandated) use cases of payments initiation and account access are just the beginning. Even now, companies are starting to develop premium APIs that “go above and beyond what is mandated,” said Homer. Some premium APIs, for example, have been designed to help with real-time credit decisioning.

With so much potential for open banking, it is worth considering what challenges exist as this promising transformation scales; some issues have already starting to surface. Sloane offered one example of how Wells Fargo reported that its middleware system was almost overwhelmed by the amount of calls its API received after being launched.

Homer noted that the metrics he has seen indicate that there is still work to be done to improve availability and uptime, especially in the U.K. There are also issues with unpredictable latency, which can lead to transaction timeouts or declines.

Controlling the data is essential

Another area of concern is with the control and security of the data itself. When using the public internet, companies run the risk of cyber threats such as distributed denial of service attacks, explained Homer. “You have created a very large attack surface by making your API to all of the customer data available on the public internet, and bad actors are going to try every way possible to figure out how to hack into that.”

Because of this, some companies have embraced private networks. Homer outlined how current rail providers—including SWIFT, Visa, and The Clearing House—have not built their connectivity to key participants over the public internet, instead electing to use private networks. This affords them granular controls of who is accessing what data and when.

Equinix is helping interconnect the open banking ecosystem

Since problems are arising as open banking scales, companies such as Equinix, with years of experience scaling complex infrastructure, are setting their sights on facilitating the rise of open banking.

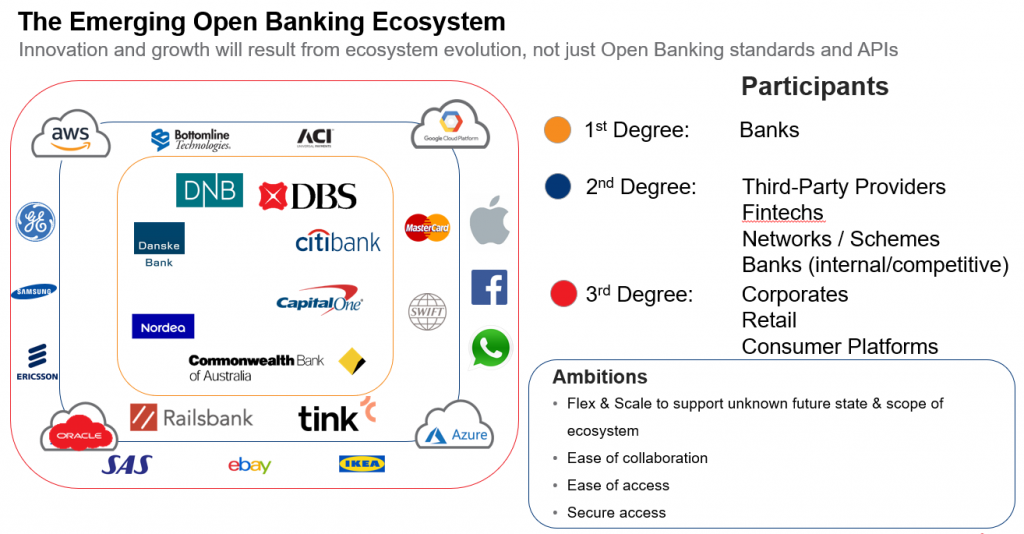

“Equinix has been focused on helping interconnect the open banking ecosystem partners so that open baking can scale overcoming the challenges of public internet,” said Homer. He described how Equinix is working to create a hybrid multi cloud world with a complex set of participants.

At the center of this ecosystem are the banks, which in turn are connected to third-party providers, including fintechs, other banks, and traditional scheme providers. Some of these parties are collocated within the Equinix infrastructure, while others exist in public clouds but have private on-ramps in Equinix. Then there is an outer ring where Equinix expects corporates and retailers to connect into the ecosystem.

“We protect, connect, and empower the mission critical assets that run today’s digital economy”

Equinix built a product called Equinix Cloud Exchange Fabric™ to facilitate such an ecosystem. The product is a private software defined network that will allow participants to exchange data such as open banking with each other in a secure fashion.

“This provides users with a secure network that they can meet the latency and availability requirements needed for open banking to scale,” said Homer.

As Homer succinctly summarized it: “What Equinix does is we protect, connect, and empower the mission critical assets that run today’s digital economy and open banking is part of that digital economy.”

What is the end state of open banking?

Homer predicted that one likely end state of open banking involves payment hubs. He explained that Equinix is witnessing the emergence of payment hubs within its ecosystem. Creating a central point where a company can communicate with other parties and handle all aspects of the payments lifecycle enables companies to achieve a digital edge, explained Homer.

Many traditional service providers are now offering these payment hubs as a service within the Equinix ecosystem. Similarly, many fintechs are deploying payment hubs as well, having realized that in order to strike a deal with a large bank, the bank’s security department will require private connectivity.